Canada Recovery Benefit (CRB)

The Canada Recovery Benefit (CRB) gives income support to employed and self-employed individuals that reside in Canada and who are directly affected by COVID-19 and are not entitled to Employment Insurance (EI) benefits. If you receive the CRB, it may impact your taxes, as described here. One key aspect is that you will have to reimburse $0.50 of the CRB for every dollar of net income you earned above $38,000 on your income tax return. Your net income (line 23600 of your tax return) can be reduced by making an RRSP deduction. Therefore, if you received the CRB and your income is above $38,000, making an RRSP deduction may allow you to keep more of the Canada Recovery Benefit payments.

If you have received the CRB, enter the amount you received for the 2020 calendar year in the "CRB income" section of the form. Do not include it as part of your income.

Example:

Let's look at an example of Pat earning $40,000 a year, living in Ontario with 1 child under 5, has $7,000 of RRSP room and received $4,000 in 2020 from the Canada Recovery Benefit.

Case 1: Pat does not put any money into her RRSP

In this case, since Pat earned over $38,000 before receiving the CRB, she needs to pay back $0.50 for every dollar above that amount. Since she earned $2,000 over the threshold, she needs to pay back $1,000.

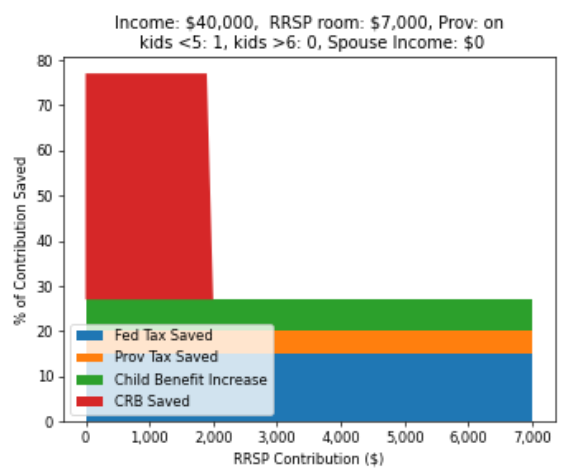

Case 2: Pat puts $2,000 into her RRSP

Pat had a tough year, and not much cash available. She had $7,000 of RRSP room available, and couldn't come up with that much money. However, she was able to use $2,000 of her RRSP contribution room. As shown in the chart below generated using the RRSP Contribution Calculator, she actually gets 77% of the $2,000 back through paying less taxes and receiving higher government benefits. By reducing her net income from $40,000 to $38,000 with her $2,000 contribution, she no longer had to pay the $1,000 back from the CRB, as in case 1.

The reduction in net income also meant she reduced her income taxes owed, and also increased her Canada Child Benefit (CCB) payments. These items combined meant she essentially got back 77% of her $2,000, or $1,540. This means that her near term cash flow is only down $460, and not the full $2,000 contribution.

On top of that, she has $2,000 in her RRSP that can grow until retirement.

Summary

| Case | RRSP Contribution | Near Term CashFlow | Comments |

|---|---|---|---|

| 1 | $0 | -$1,000 | Have to pay back $1,000 and no money added to RRSP |

| 2 | $2,000 | -$460 | Out less cash near term than Case 1, and has $2,000 added to RRSP |

Although it was tough for Pat to find the money for the RRSP contribution, after accounting for her tax refund and higher benefits, she not only had more cash in the near term, but more money in her RRSPs.